Free cash flow (FCF) is defined as the cash a company generates after paying for its operating expenses and capital expenditures, representing true cash profitability beyond what accounting profits show. Unlike net income, FCF strips away non-cash adjustments and accruals, giving investors a cleaner picture of what a business actually produces. The CFA Institute and professional valuation analysts treat FCF as a cornerstone metric in fundamental analysis. For individual investors and finance students, mastering FCF is the difference between evaluating a company on paper profits and understanding its real financial strength.

What is free cash flow and why does it matter?

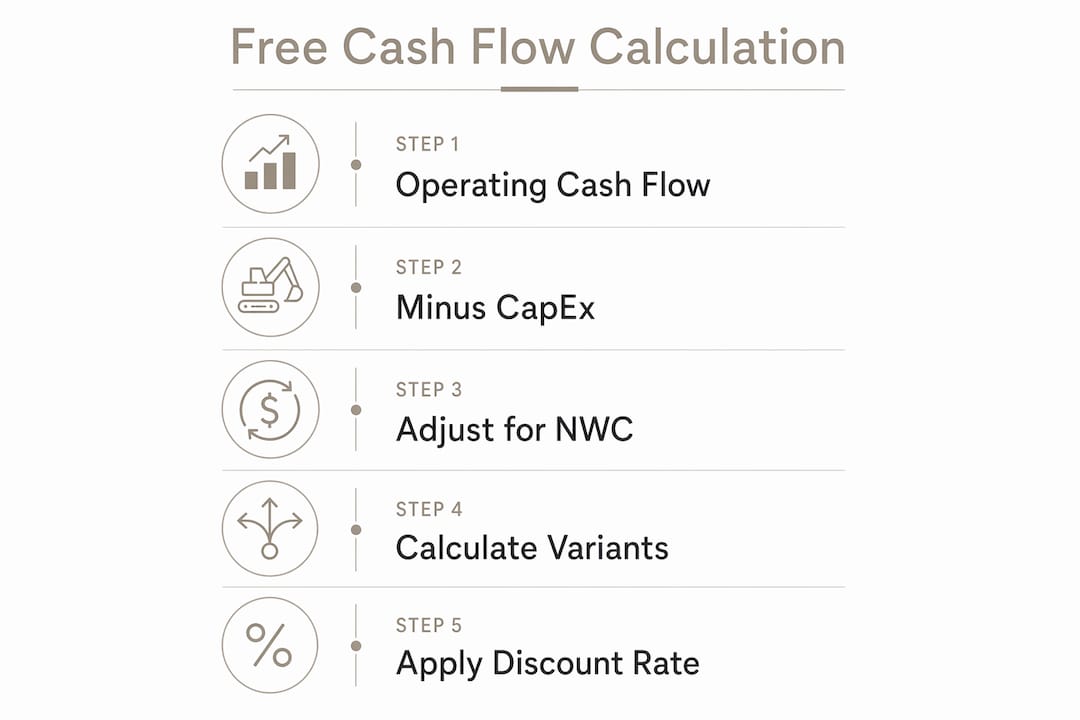

Free cash flow is the cash left over after a company funds its operations and reinvests in its assets. The standard FCF formula is Operating Cash Flow minus Capital Expenditures. Operating Cash Flow comes from the operating activities section of the cash flow statement. Capital Expenditures appear in the investing activities section. This single calculation tells you how much cash a business generates that it can use for dividends, debt repayment, acquisitions, or share buybacks.

The importance of free cash flow goes beyond its formula. Net income can be positive while a company burns through cash. FCF cannot be dressed up the same way because it tracks actual dollars moving in and out of the business. That is why Warren Buffett, Charlie Munger, and Peter Lynch all built their investment frameworks around cash generation rather than reported earnings.

How to calculate free cash flow: formulas and variants

The shortcut formula, Operating Cash Flow minus CapEx, works for a quick read. For serious valuation work, you need to understand the three primary FCF variants: unlevered free cash flow (FCFF), levered free cash flow (FCFE), and owner earnings.

The three main FCF variants

| Variant | Formula summary | Discount rate | Primary use case |

|---|---|---|---|

| FCFF (Unlevered) | EBIT × (1 – tax rate) + D&A – CapEx – change in NWC | WACC | Enterprise value for entire firm |

| FCFE (Levered) | Net income + D&A – CapEx – change in NWC + net borrowing | Cost of equity | Equity value; common for banks |

| Owner earnings | Net income + D&A – maintenance CapEx | Cost of equity | Intrinsic value per Buffett's method |

FCFF discounts at the Weighted Average Cost of Capital (WACC) to produce enterprise value. You then subtract net debt to reach equity value, and divide by shares outstanding to get intrinsic value per share. FCFE discounts at the cost of equity and is most common for financial firms where debt is part of the operating model. Owner earnings, popularized by Warren Buffett, focuses only on maintenance CapEx, the spending required to keep the business running at its current level.

Pro Tip: When you build a DCF model, always match your FCF variant to your discount rate. Using FCFE with WACC, or FCFF with cost of equity, produces a fundamentally wrong valuation.

Locating these inputs is straightforward. Open the cash flow statement and find "cash from operating activities" for the operating cash flow figure. Find "purchases of property, plant, and equipment" in the investing section for CapEx. Changes in net working capital appear either as line items within operating activities or in the balance sheet comparison between two periods.

Why FCF beats net income and EBITDA for investment analysis

Net income includes non-cash charges like depreciation, amortization, and stock-based compensation, plus accrual-based revenue recognition that can shift income between periods. FCF reflects actual cash generation and is far less susceptible to manipulation through accounting choices. A company can report growing net income for years while its cash position deteriorates. FCF exposes that gap immediately.

EBITDA is even further removed from reality for capital-intensive businesses. It adds back depreciation and amortization but ignores capital expenditures entirely. A steel manufacturer or semiconductor company spending billions on equipment every year looks far healthier on an EBITDA basis than its cash position justifies. FCF accounts for that reinvestment directly.

Free cash flow is the metric that tells you whether a business is actually creating value or just reporting it. A company that consistently converts earnings into cash is a fundamentally different animal from one that cannot. Investors who rely solely on net income or EBITDA miss this distinction entirely.

- Net income distortions: depreciation, amortization, deferred taxes, and stock compensation all inflate reported earnings without producing cash.

- EBITDA blind spots: ignores CapEx, working capital changes, and interest payments, making it unreliable for capital-heavy industries.

- FCF advantages: cash-based, harder to manipulate, directly tied to what stakeholders can actually receive.

Negative FCF is not automatically a red flag. A high-growth company investing heavily in new capacity or market expansion may run negative FCF for years while building enormous future value. Amazon did exactly that through most of the 2000s. The key question is whether the reinvestment is generating returns above the cost of capital.

Common pitfalls in FCF calculation and interpretation

The shortcut formula (Operating Cash Flow minus CapEx) is widely used but carries real risks. Practitioners reconcile FCF starting from EBIT or Net Income to avoid inflated figures caused by non-cash charges and complex financing structures. Skipping that reconciliation step can make a company look far more cash generative than it actually is.

Key calculation errors to avoid

- Ignoring delta NWC: Changes in net working capital can falsely signal cash generation. A spike in accounts receivable means revenue was recognized but cash was not collected. That difference must be subtracted from FCF.

- Mixing maintenance and growth CapEx: Separating maintenance CapEx from growth CapEx is central to calculating owner earnings accurately. Lumping them together understates the cash truly available to owners.

- Ignoring net borrowing in FCFE: FCFE includes net borrowing adjustments because debt raised or repaid directly affects cash available to equity holders. Omitting it gives a distorted equity value.

- Treating all negative FCF equally: Negative FCF can indicate healthy reinvestment for growth companies. Context determines whether it signals strength or stress.

Pro Tip: Reconcile your FCF calculation from EBIT using this path: EBIT × (1 – tax rate) + D&A – CapEx – change in NWC. This method forces you to account for every major cash driver and avoids the inflation risk of starting from operating cash flow directly.

The table below shows how each adjustment changes your FCF figure and what it signals.

| Adjustment | Effect on FCF | What it signals |

|---|---|---|

| Rising accounts receivable | Reduces FCF | Cash not yet collected from customers |

| Rising inventory | Reduces FCF | Capital tied up in unsold goods |

| Maintenance CapEx increase | Reduces FCF | Higher cost to sustain current operations |

| Net borrowing (positive) | Increases FCFE | New debt raised, boosting equity cash |

| Large growth CapEx | Reduces FCF | Expansion investment, not a cash drain per se |

How investors use FCF in valuation and investment decisions

FCF is the input that powers discounted cash flow (DCF) valuation models. DCF models forecast FCF over 5–10 years and discount those cash flows back to present value using the appropriate rate. The result is an estimate of intrinsic value that you can compare directly to the current market price.

Choosing the right FCF variant matters enormously for this process. Investors must match their FCF variant to their valuation focus: FCFF for the entire firm, FCFE for equity holders alone. Using the wrong variant with the wrong discount rate produces a number that looks precise but is fundamentally wrong.

Beyond DCF, FCF analysis reveals capital allocation quality. A company that generates strong FCF and deploys it into high-return investments, share buybacks at attractive prices, or debt reduction is demonstrating financial discipline. A company that generates strong FCF but destroys it through poor acquisitions or excessive executive compensation tells a different story entirely.

Price-to-FCF multiples are less standardized than P/E ratios, partly because FCF volatility from reinvestment cycles makes year-to-year comparisons difficult. That volatility is real, but it does not diminish FCF's value. It means you need to look at FCF trends over three to five years rather than a single year snapshot.

For a practical framework on applying these concepts, the owner earnings approach explained by Oracleinvestments connects FCF directly to intrinsic value scoring in a way that individual investors can apply immediately.

Key Takeaways

Free cash flow is the most reliable measure of a company's true cash profitability, and matching the right FCF variant to the right discount rate is the single most important step in accurate valuation.

| Point | Details |

|---|---|

| FCF definition | Cash remaining after operating expenses and capital expenditures, not accounting profit. |

| Three FCF variants | Use FCFF for firm value, FCFE for equity value, and owner earnings for intrinsic valuation. |

| FCF vs. net income | FCF is harder to manipulate because it tracks actual cash, not accrual-based earnings. |

| Calculation pitfalls | Always adjust for delta NWC, separate maintenance from growth CapEx, and reconcile from EBIT. |

| Negative FCF context | Negative FCF signals reinvestment in growth companies; sustained negative FCF in mature firms is a warning. |

Why FCF mastery changed how I evaluate every stock

Most investors learn the shortcut formula and stop there. That is a mistake I made early on, and it cost me real money. I once evaluated a mid-cap retailer that showed strong operating cash flow and modest CapEx on the surface. The FCF looked healthy. What I missed was a steady buildup in inventory and receivables that was quietly consuming cash. The delta NWC adjustment would have flagged it immediately. The stock dropped 40% the following year when the cash crunch became undeniable.

The lesson is not that FCF is complicated. The lesson is that the shortcut formula rewards lazy analysis. When you take the time to reconcile from EBIT, separate maintenance from growth CapEx, and track working capital changes, you see things that most market participants miss. That gap is where real investment edge lives.

I also want to push back on the idea that negative FCF is always a problem. Some of the best investments I have studied ran deeply negative FCF for years because they were building infrastructure that would generate cash for decades. The question is always whether the reinvestment earns a return above the cost of capital. If it does, negative FCF is a feature, not a bug. If it does not, even positive FCF cannot save a bad business.

Combine FCF analysis with qualitative research on management quality, competitive positioning, and industry dynamics. Numbers tell you what happened. Qualitative work tells you why and what comes next. The investors who do both consistently outperform those who rely on either alone.

— Matt

Putting FCF analysis to work with Oracleinvestments

Understanding FCF formulas is one thing. Applying them across dozens of stocks quickly and accurately is another challenge entirely.

Oracleinvestments scores over 260 stocks on key financial fundamentals including profitability, valuation, and financial health, incorporating owner earnings and intrinsic value concepts directly into its ratings. The platform draws on the investment frameworks of Warren Buffett, Charlie Munger, and Peter Lynch, translating FCF-based analysis into clear, comparable scores that individual investors can act on. Whether you are screening for undervalued companies or tracking your existing portfolio, Oracleinvestments gives you the analytical depth of a professional research desk without the complexity. Explore the Oracleinvestments blog for deeper coverage of valuation methods, FCF variants, and stock analysis frameworks.

FAQ

What is the basic free cash flow formula?

Free cash flow equals Operating Cash Flow minus Capital Expenditures. Both figures come directly from the cash flow statement: operating cash flow from the operating section, and CapEx from the investing section.

What is the difference between FCFF and FCFE?

FCFF (unlevered free cash flow) represents cash available to all capital providers and is discounted at WACC to find enterprise value. FCFE (levered free cash flow) represents cash available only to equity holders and is discounted at the cost of equity.

Why is free cash flow better than net income for evaluating stocks?

Net income includes non-cash items like depreciation and accrual-based revenue that can distort earnings. FCF tracks actual cash generated, making it harder to manipulate and more directly tied to the value a company delivers to shareholders.

Can a company have positive net income but negative free cash flow?

Yes, and it happens frequently. Heavy capital expenditure cycles or rising working capital needs can consume cash even when reported earnings look strong. This divergence is one of the most important signals FCF analysis reveals.

What does negative free cash flow mean for investors?

Negative FCF is not automatically a warning sign. Growth companies reinvesting heavily in capacity or market expansion often run negative FCF for years. The key is whether those investments generate returns above the cost of capital over time.